Despite the socio-political unrests and economic volatility in 2020, residential property markets in global gateway cities (like Singapore and London) have been largely resilient. These markets remain active with demand coming from investors who seek stable assets that offer predictable returns.

For Asian societies, we recognise the value of real estate to be one of the most resilient asset classes and a natural hedge against inflation. With it comes the track record of strong long-term performance and ability to generate a passive income stream.

Becoming a landlord and generating positive monthly cash flow from property rentals is an approach that most Singaporeans have benefitted from. However, with rising housing prices and high capital values of properties in Singapore today, is a positive cash flow still achievable?

Looking Beyond

Sophisticated investors choose to venture into international markets to diversify the risks that come with owning local investment properties. A common approach is to capitalise on gateway cities, such as London. The British city remains a favourite among Singaporeans, largely due to the similar spoken national language and legislations that are widely enforceable and recognised.

Home to one of the world’s leading financial hub and some of the best universities, London holds a strong global talent pool. Considering its rich culture, unique urban fabric and quintessential British lifestyle, it’s no surprise people love the city.

Singapore & London – What’s the Difference in Terms of Financing Options?

While similar in potential for investment returns, what sets Singapore and London apart is the financing options available. This drastically affects the monthly cash flow value of properties. On top of the typical repayment loan (Principal + Interest) option available in Singapore, London offers financing via the Interest-Only Loan.

With an Interest-Only loan, only a portion of the interest on the loan is required. This results in lower monthly payments for a fixed period, which will likely give you the benefit of having positive monthly cash flow returns from your investment property.

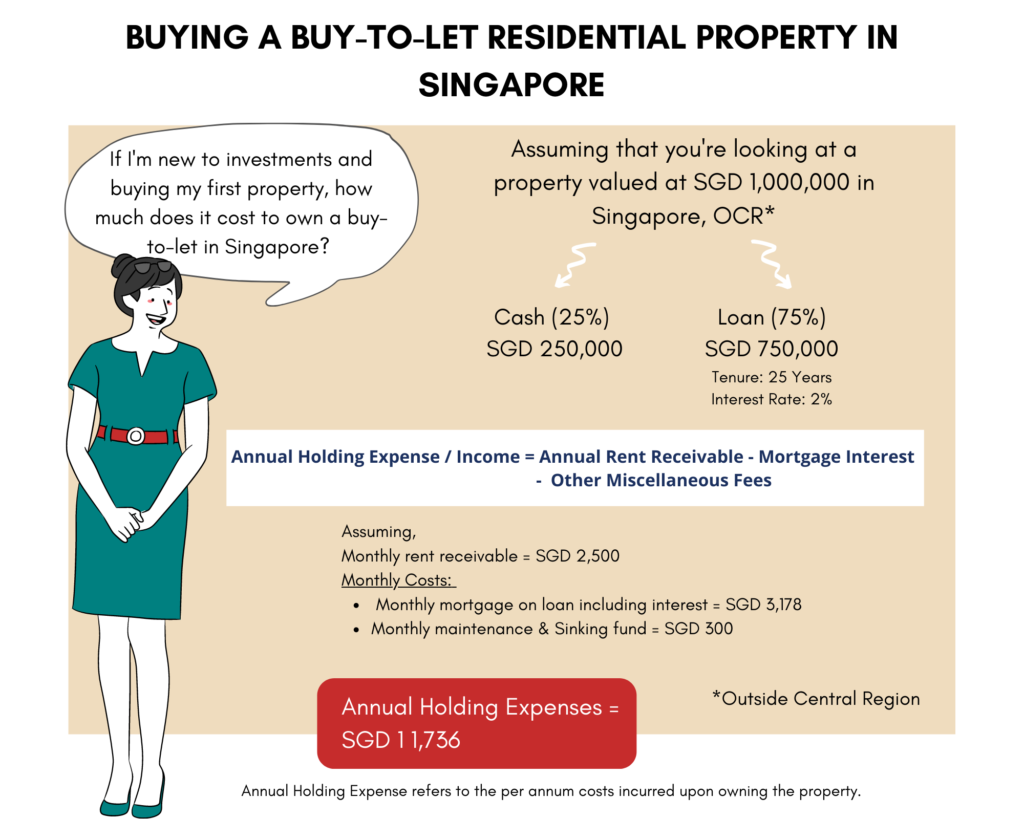

The figure below shows a comparison between two different investment properties in Singapore and London, based on the assumption of a SGD 1 million price point that affords an investor a 1-bedroom apartment in the Rest of Central Region (RCR) Singapore, or a 1-bedroom in Zone 1 and Zone 2 London.

By choosing a suitable loan financing appetite, an investor is able to, on average, purchase a buy-to-let 1-bedroom apartment located in RCR Singapore that incurs SGD 11,736** holding cost annually, whereas a property in London with a similar price point in Zone 1 and Zone 2 that typically generates SGD 4,877 annually.

** for illustration only

It All Boils Down to Intent

When deciding on the most suitable option, it is an investor’s responsibility to factor in personal commitments and preferences over a reasonable investment horizon.

While the Interest-Only loan is attractive and unavailable in Singapore, you are still required to pay off the full principal amount upon the loan deadline.

An Interest-Only loan might make more sense for an investor who has a shorter time horizon, whereas the repayment loan option might be more suitable for investors who prefer to hold the property long-term. It all comes down to rebalancing your equity, debts and assets on your personal balance sheet.